Home › Forums › Trading Courses › Forex Strategy Course + 12 EAs I Trade Live › Forex strategy course – Portfolio trading with 12 Expert Advisors – Questions

- This topic has 21 replies, 1 voice, and was last updated 5 years, 9 months ago by

Petko Aleksandrov.

Petko Aleksandrov.

-

AuthorPosts

-

-

July 27, 2019 at 0:32 #16906

SimonParticipant

SimonParticipantHi Petko,

I have a few questions regarding the Forex strategy course – Portfolio trading with 12 Expert Advisors

I thought it might be a good idea to start a thread on it, so others can ask questions here too..

Here goes..

1) In video “02. How we collect and update the historical data” you mention collecting data every month, and adding it to the data you collected before, and keep in an Excel spreadsheet, but I wonder why we can’t simply set the MT4/MT5, chart properties, or indeed the Export data script to have maximum 300,000 bars, and we just use that data? Why keep old data, and spend time copy/pasting?

What you say about using current data rather than an enormous amount make good sense to me.

2) How many bars should we use for each timeframe?

M1: 300,000 bars

M5: ?

M15: ?

M30: ?

H1: ?

and so on..

Thanks,

Simon

-

July 28, 2019 at 19:11 #16994Petko AleksandrovKeymaster

Hey Simon,

this was because many people wanted to use many bars. Like 500 000 and more. There are traders who want to test EAs for the last 10 years. Personally, I think it is not necessary, but I showed a method of how they can collect it.

On the higher time frames, I would use more….for example what is in the MetaTrader-Demo server in EA Studio is good:

M1: 300,000 bars

M5: 200,000 bars

M15: 100,000 – 120,000 bars

M30: 50,000 – 60,000 bars

H1: 25,000 – 30,000 bars

Cheers,

-

July 28, 2019 at 22:49 #17008SimonParticipant

Thank you for the reply!

-

July 30, 2019 at 17:17 #17095Petko AleksandrovKeymaster

Cheers, Simon!

Just keep in mind that the more bars you use you will have more count of trades, which will make the strategies more robust.

At the same time, if you use more bars you are lowering the profit per day.

So something in the middle is always the best.

-

July 30, 2019 at 22:44 #17108SimonParticipant

Thanks Petko.

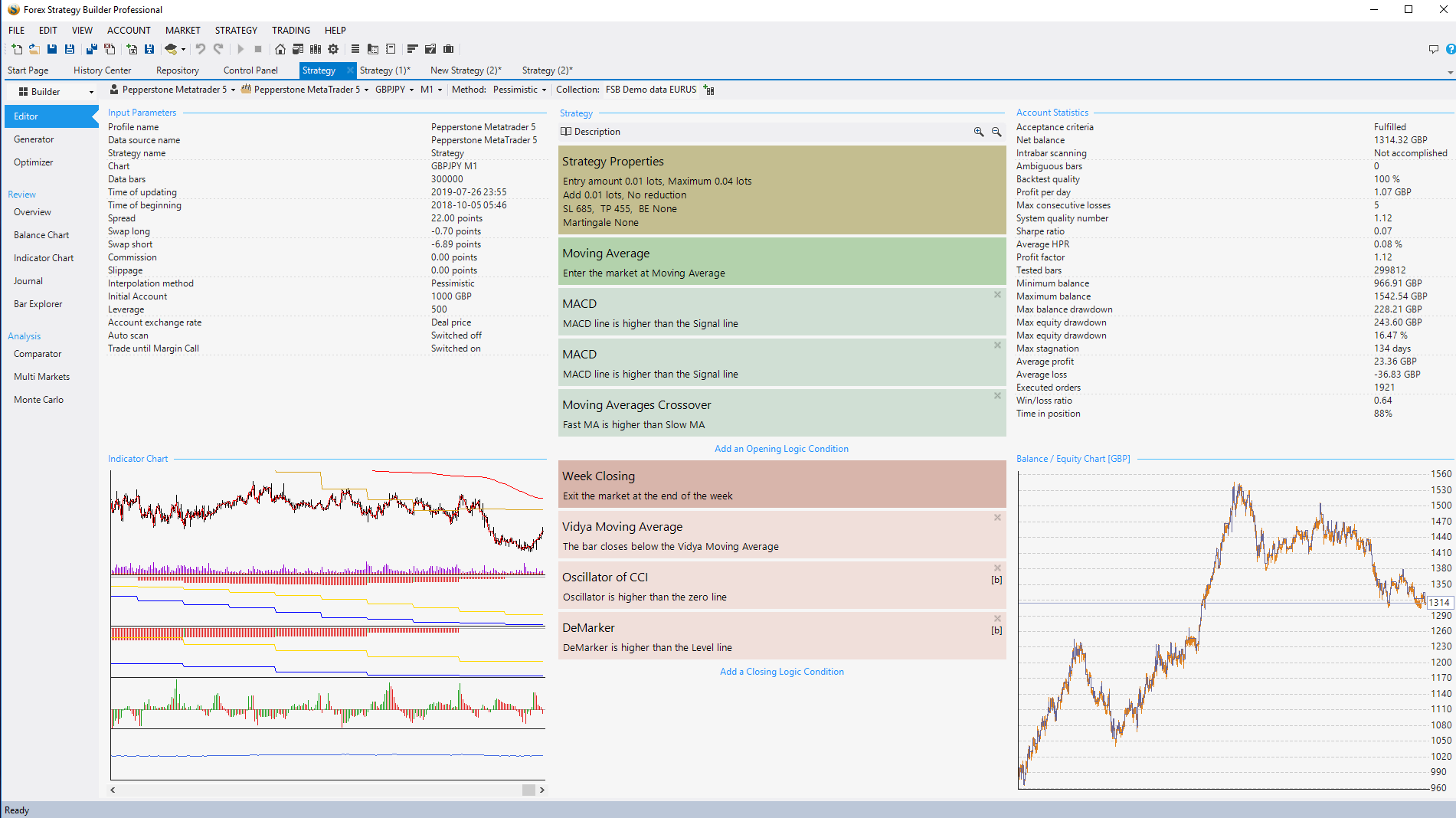

I’ve been running the generator as per the course for roughly ten hours at a time, and rarely find any strategies, but I did find this one:

It didn’t look very nice, to be honest, but I followed the optimization instructions in video 09. FSB Pro – Longer time frames 1.1, and applied what I could to my strategy, given that it has different indicators, and honestly, I am guessing at what effect the parameters have on the strategy, and finished up with the following:

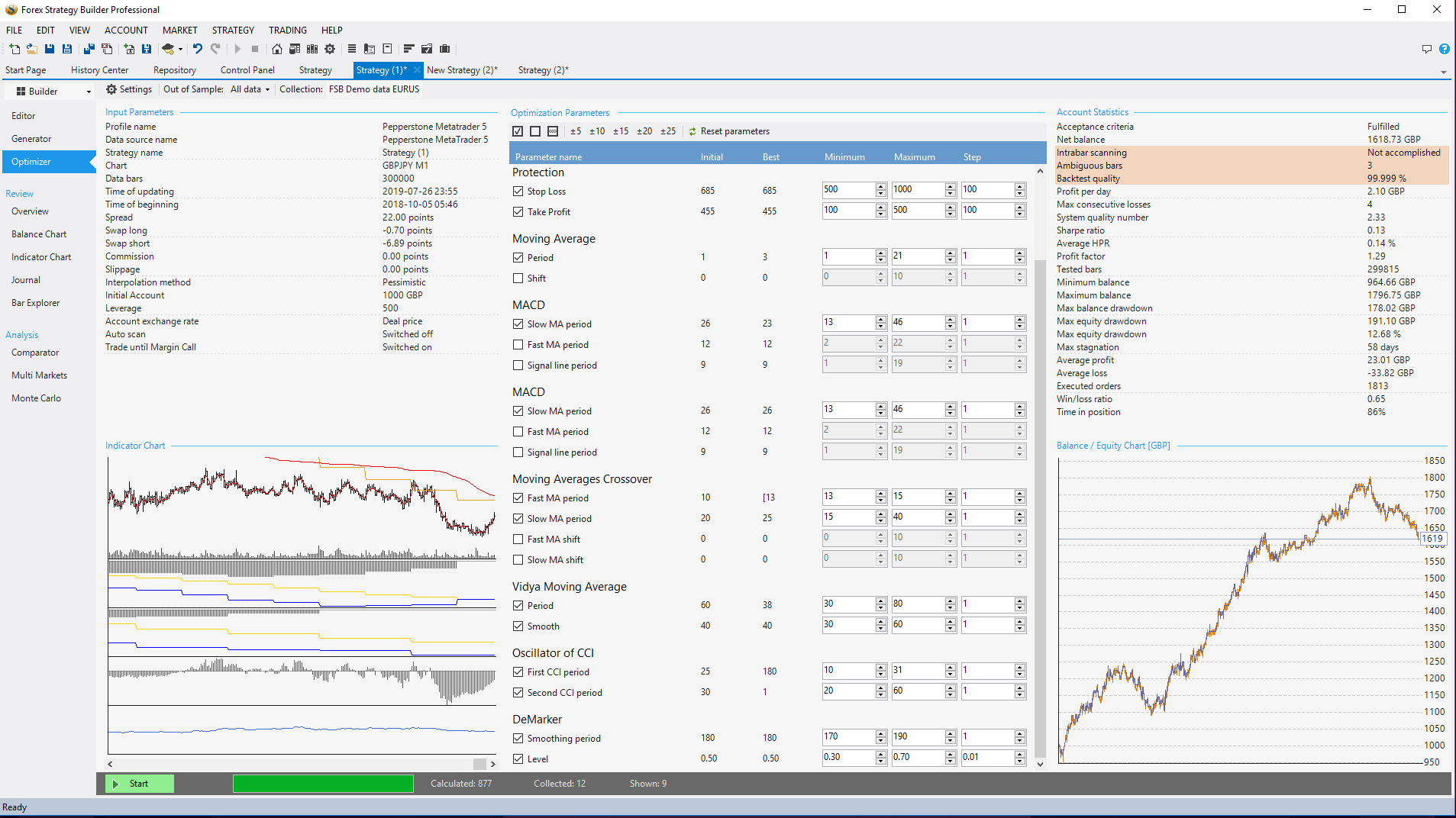

The Net Profit is better, and the equity curve has smoothed out a bit, but I don’t like that it is still losing money most recently. Would you bother testing this on a demo account?

I’m not sure if you can determine much from this screenshot, I entered the parameters into the Optimizer as best I could after watching the above video, but is there anything you would have done differently?

If I’m not able to generate many strategies, should I get rid of some of the locked logical conditions? They are as per your suggestions in video 04. FSB Pro – Longer time frames 1

I’ve had the acceptance criteria set to:

Minimum profit per day – 1

Minimum count of trades – 300

Is this too strict?

Cheers,

Simon.

-

August 1, 2019 at 11:42 #17208Petko AleksandrovKeymaster

Hey Simon,

I think you are doing a good job. This is exactly what you need to do…experiment, test and progress…

Now, regarding this strategy, I think you have a lot of exit conditions. Try to remove at least 2, and repeat the optimization. See if this will bring you better profits. I do not like having the strategies losing recently but if you look at its equity line there was such a period in the beginning. So yes, it worths testing it.

But once again, try to remove a few of the Exit conditions. they might limit the optimizer for finding better parameters at the end.

-

August 9, 2019 at 15:35 #17677SimonParticipant

Hi Petko,

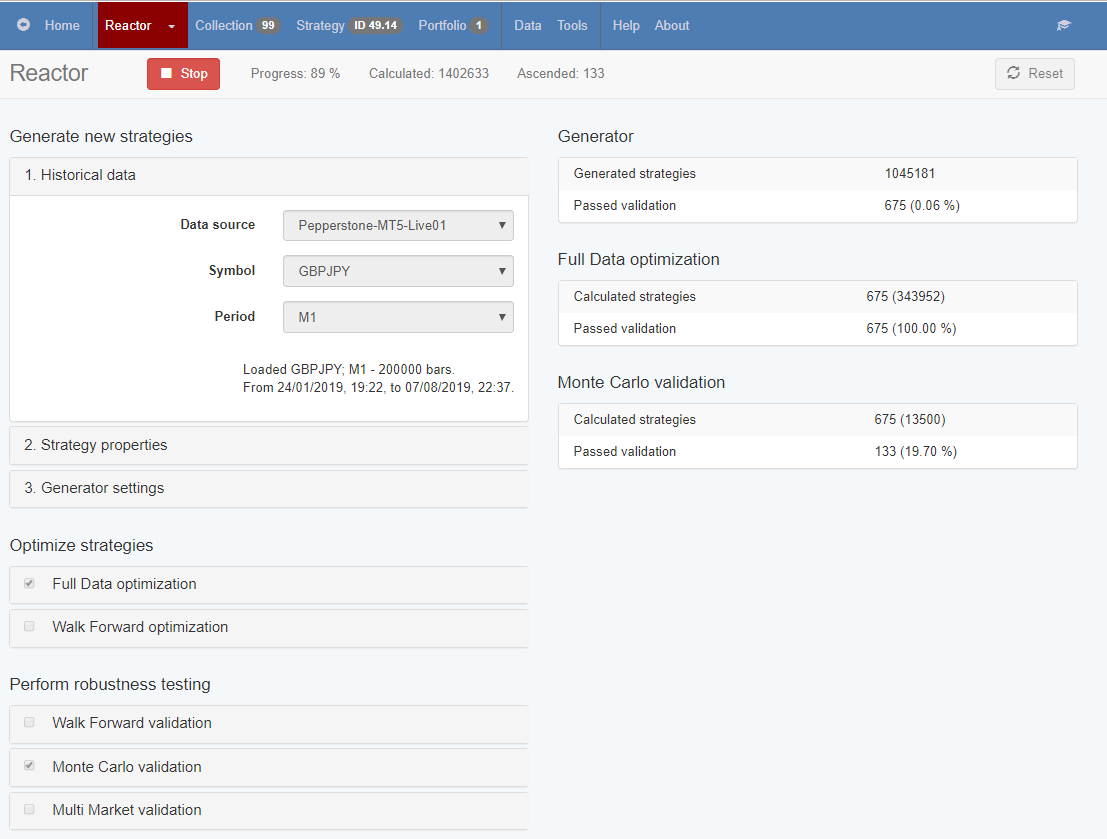

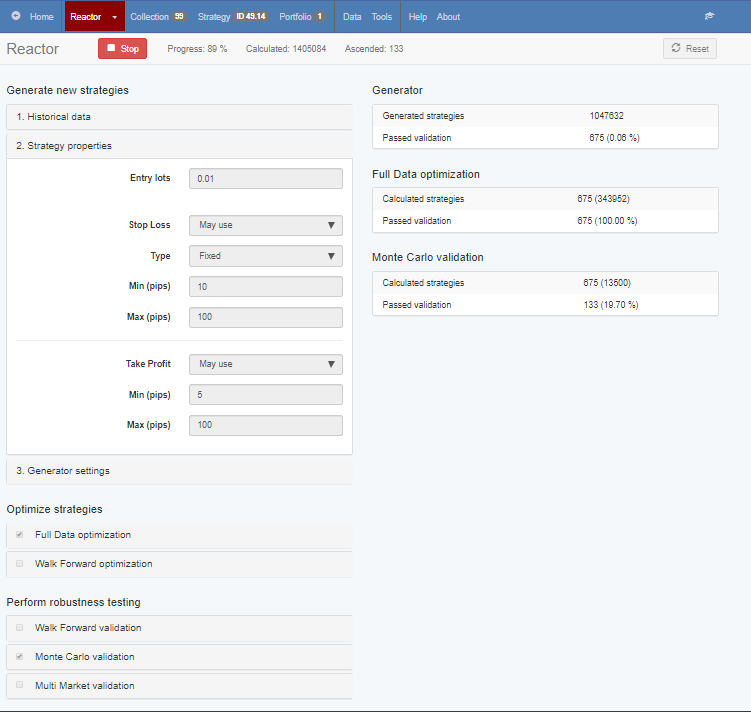

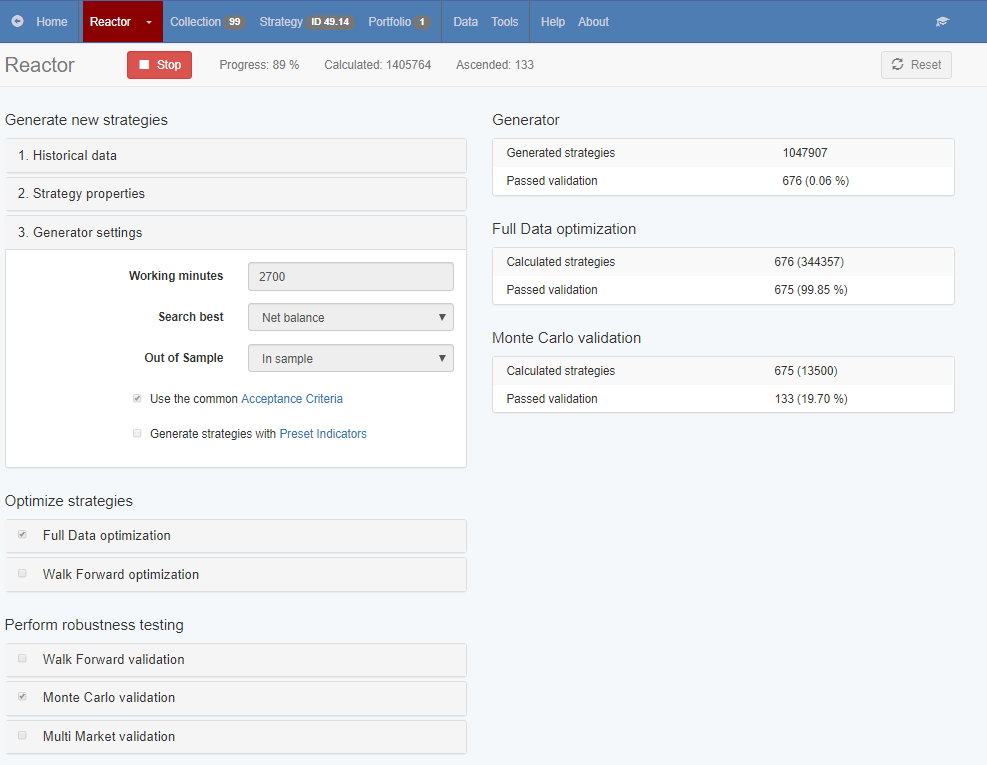

I’ve been following the instructions as per the video: 12. The Reactor, and running it for nearly two days now, and have a collection of 100 strategies to work with.

Screenshots of the settings are as follows:

Historical Data settings

Strategy Properties settings

Generator Settings

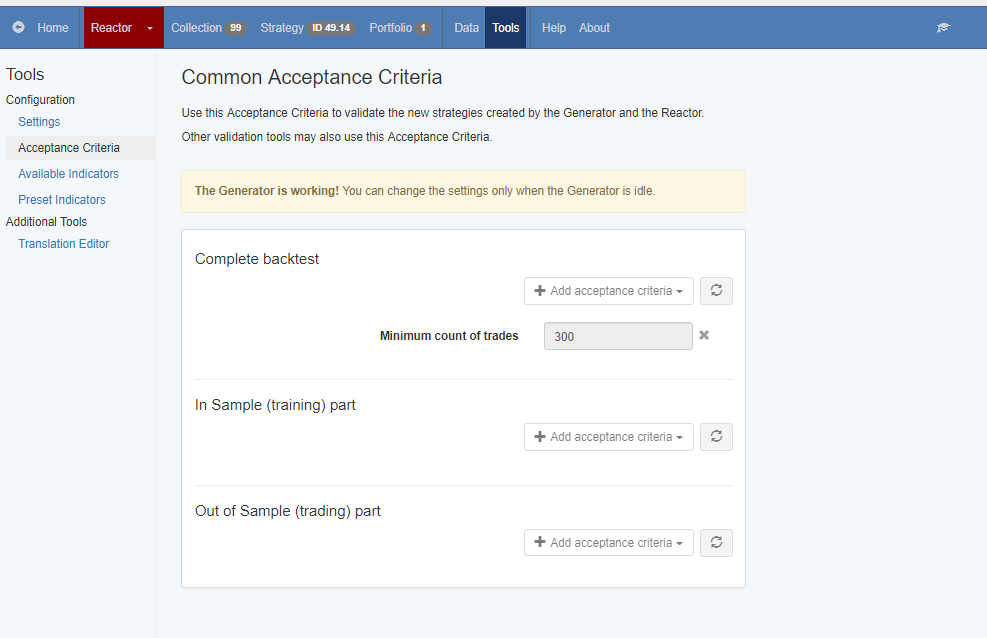

Acceptance Criteria settings

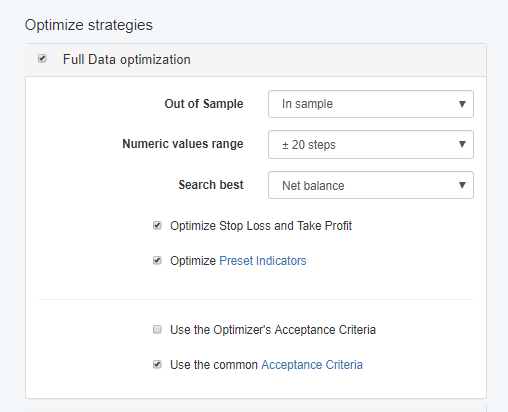

Optimize Strategies settings

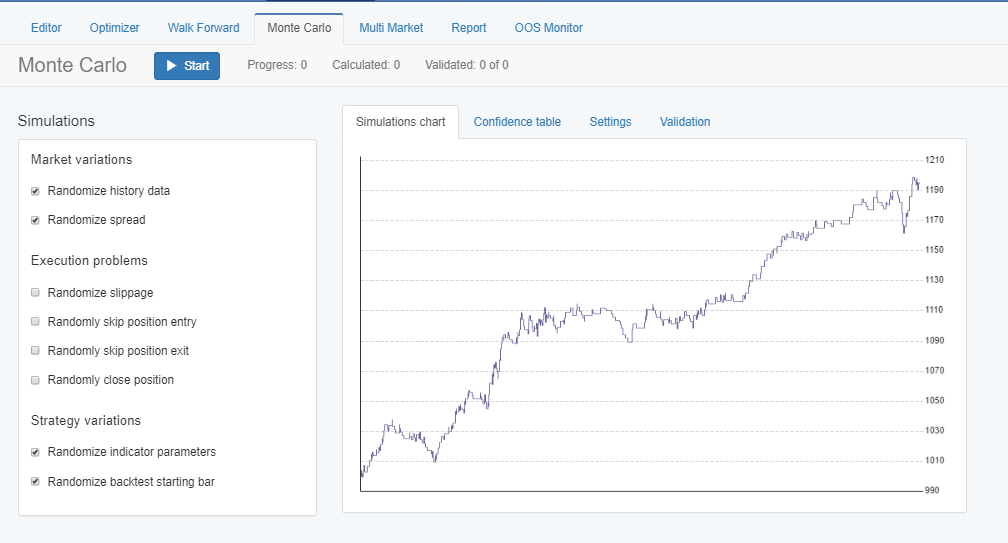

Monte Carlo settings

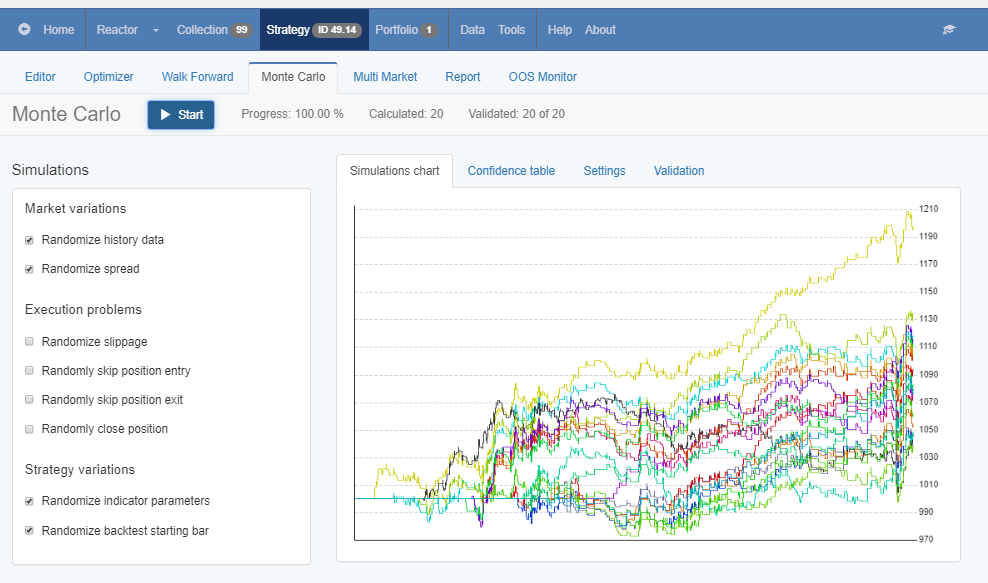

Monte Carlo results

Can you see anything I should have done differently?

Are the Monte Carlo results above acceptable? When are they not acceptable?

Should I now filter these using the performance filters?

Perhaps get the Maximum Stagnation percentage as low as possible?

Or, seeing that they have all passed the Reactors requirements, should I put them all of a demo account and see how they perform?

Thanks,

Simon

-

August 10, 2019 at 17:05 #17748Petko AleksandrovKeymaster

Hello Simon,

Glad to hear from you, and nice you post pictures, this way I can assist the most.

Now, the Monte Carlo is totally acceptable. As you can see there 20 out of 20 test validated(this is 100%).

I would increase a bit more the number of trades in the Acceptance criteria. I see you have 200k bars which allow you to request more bars.

The other thing is that I am not really a fan of using Full data optimizer. You have really the risk to over-optimize the strategies. Yes, you run the Monte Carlo, but still…I am just not a fan of it. If you find these strategies profitable in the future as well, then you are fine. Give it a try.

Normally, I would filter them a bit more. Recently I use more and more the min count of trades. I would just squeeze them to get the strategies with the most number of trades.

Let me know if there is anything else.

Cheers,

-

August 10, 2019 at 18:06 #17753SimonParticipant

Thanks for the reply Petko.

I am looking now at the Walk Forward Optimization course, and trying to figure out which elements of that I could apply to the Reactor settings.

I have just finished watching the OOS lecture, which looks very useful, but I remember in another video that you said you weren’t a fan of it, so currently a little confused about what to try..

I really like the idea of having the Reactor do as much work as possible, being that I have another business to run, and family matters needing attention. What is your current view of a good chain of settings for it to generate and validate robust strategies that require no more work, other than testing in a demo MT4/5 account? I understand that you are not a fan of Full Data Optimization, but perhaps I should concentrate more on the OOS and Walk Forward sections of the Reactor? Multi-Market too?

For the sake of keeping it simple, I am just focusing on GBPJPY M1 at the moment, if I found a Reactor setup that works for that, would the same setup work for other symbols and timeframes?

Re the number of bars, I only used 200,000 this time because it allows the Reactor to run more quickly, perhaps I could increase it to 300,000 bars and go for 30% OOS, to give the Reactor a similar chance to generate strategies, with the OOS section there to simulate the trades on?…

Cheers,

Simon

-

August 12, 2019 at 10:23 #17835Petko AleksandrovKeymaster

Hey Simon,

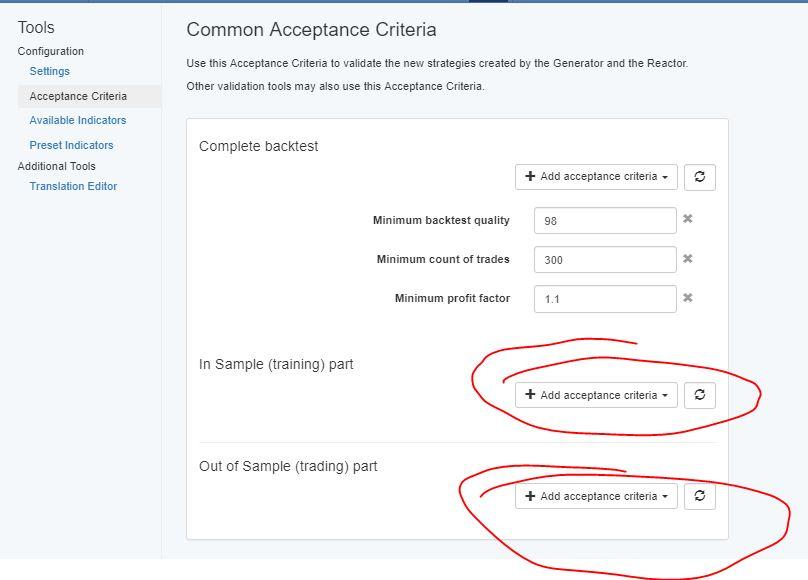

yes, you are correct, I was not a fan of it before. But it changed after the Acceptance criteria were updated with In Sample and Out of Sample options. This way we can choose criteria for both:

This is totally different now. Before we had it only for the complete backtest. Now, we can choose for both of the segments. This way we can filter in the Reactor the strategies that are profitable in the Out of Sample Part. And at the same time, we really test those on unknown data.

I understand you want to keep it simple and less work, everyone wants that for sure :) However, concentrating on one currency pair is not really a good risk-diversification. Try to do at least three different assets. Also, on M1 you would like to trade the currencies that have the lowest spread, and GBPJPY is not one of those.

If you trade on M1, you can go to 300k.

Just run the reactor strictly, make sure to put Monte Carlo always to test the robustness, and look for Min Count of Trades. Increase it as much as possible.

Cheers,

-

August 13, 2019 at 0:30 #17895SimonParticipant

Thanks Petko, I see now that there have been updates to EA Studio since the videos were made.

I understand about diversifying the risk, it makes good sense. For now, I am really learning about how the software works more than anything, so will focus on different assets when I am more comfortable with it’s capabilities.

I am finding it quite confusing that so many sections in the Reactor have the option for Acceptance Criteria and OOS, I have no idea what is happening if I have a combination of sections with one or both of them switched on or off! Is it possible to cause problems if you have either of them switched on in several places?..

Is there a video that you have done that covers the said Reactor queries?

Thanks, Simon

-

August 13, 2019 at 6:48 #17908Petko AleksandrovKeymaster

Hey Simon,

Good one here about the Reactor, it was changed indeed, and I see as well that there are some changes which I believe what they mean but not really sure.

I guess the generated strategies go in a consecutive way down to the reactor, and if they pass it, it continues lower…however I am not sure about the OOS how it works in each section. If Petko can make it clearer will be great.

-

August 23, 2019 at 9:14 #18557Petko AleksandrovKeymaster

Hey guys,

I am going to record a video about the changes in the EA Studio and exactly what is the logic that OOS and Walk Forward follow when running the Reactor.

Cheers,

-

August 24, 2019 at 17:05 #18632SimonParticipant

That’s really great Petko, thank you very much!

-

August 24, 2019 at 20:27 #18641Petko AleksandrovKeymaster

I am looking forward to this video! not really sure if I do the OOS and Walk Forward optimization properly.

-

August 27, 2019 at 15:35 #18920Petko AleksandrovKeymaster

Hey Sisi, I will be recording the video today, so hopefully tomorrow we will upload it.

Cheers,

-

September 24, 2019 at 0:11 #22240SimonParticipant

Hi Petko,

I hope you are well, just wondering if you will be uploading the video on the Reactor soon?

Many Thanks,

Simon

-

September 24, 2019 at 10:35 #22264Petko AleksandrovKeymaster

Hey Simon,

Yes, I am just out of town and getting back to the office today. I will upload the updates in the course today.

Which video exactly do you mean?

-

September 24, 2019 at 20:03 #22283SimonParticipant

Hi Petko,

I have no doubt you are a busy person!

The video I mean is the one in which you kindly offered to explain the intricacies of the Reactor, now that it has so many ways to use OOS and Walk Forward. It was in this post from earlier in this thread – https://eatradingacademy.com/forums/topic/forex-strategy-course-portfolio-trading-with-12-expert-advisors-questions/#post-17895

-

September 24, 2019 at 22:23 #22288Petko AleksandrovKeymaster

Hello Simon,

Actually this video is already uploaded in the EA Studio updates:

Please, have a look at it and let me know if this is what you are looking for.

Cheers,

-

September 25, 2019 at 22:11 #22374SimonParticipant

Hey Petko,

I must have missed the update, I see you have indeed kindly made a video explaining the update to the OOS and Walk Forward parts of the Reactor, thank you very much indeed.

I will spend some time absorbing your advice.

Cheers,

Simon

-

September 26, 2019 at 23:54 #22445Petko AleksandrovKeymaster

Hey Petko, thanks for updating this course with the updated videos! It was a good thing to go over them once again!

-

-

AuthorPosts

- You must be logged in to reply to this topic.