Home › Forums › EA Studio › Reactor › Quantity of generated strategies relevant to better profitability of EA’s?

- This topic has 16 replies, 1 voice, and was last updated 5 years, 8 months ago by

Petko Aleksandrov.

Petko Aleksandrov.

-

AuthorPosts

-

-

October 28, 2019 at 15:35 #25226

Jay-r YuzonParticipant

Jay-r YuzonParticipantHi everyone,

I noticed while generating strategies using the same parameters, that some assets (currencies) have more generated strategies into the collection. By experience, might this give us a hint that the asset class that generated MORE STRATEGIES have more chances to be more profitable, at least, during the nearterm? And of course I’m asking this question with the assumption that the due diligence required in filtering the generated strategies found in the collection has already been exhausted. Just saying whether the QUANTITY of generated strategies into the collection could play a role in anticipating which asset class could perform better relative to the other asset classes that were generated using the same parameters, historical period, timeframe, etc.?

Cheers,

Jay-R

-

October 30, 2019 at 7:20 #25478Petko AleksandrovKeymaster

Hello Jay-R,

for certainty, you see different results because the Historical data of each asset is different. The behavior of the price is different so it forms the different Historical data.

what you say is quite interesting… It is correct that the most strategies we see, the more this asset is suitable for the strategies generated by EA Studio. Simply, its Historical data shows and proves that.

-

October 30, 2019 at 9:42 #25486Jay-r YuzonParticipant

I like how you described it Bart… “the more this asset is suitable for the strategies generated by EA Studio”

That’s basically what I was trying to say.

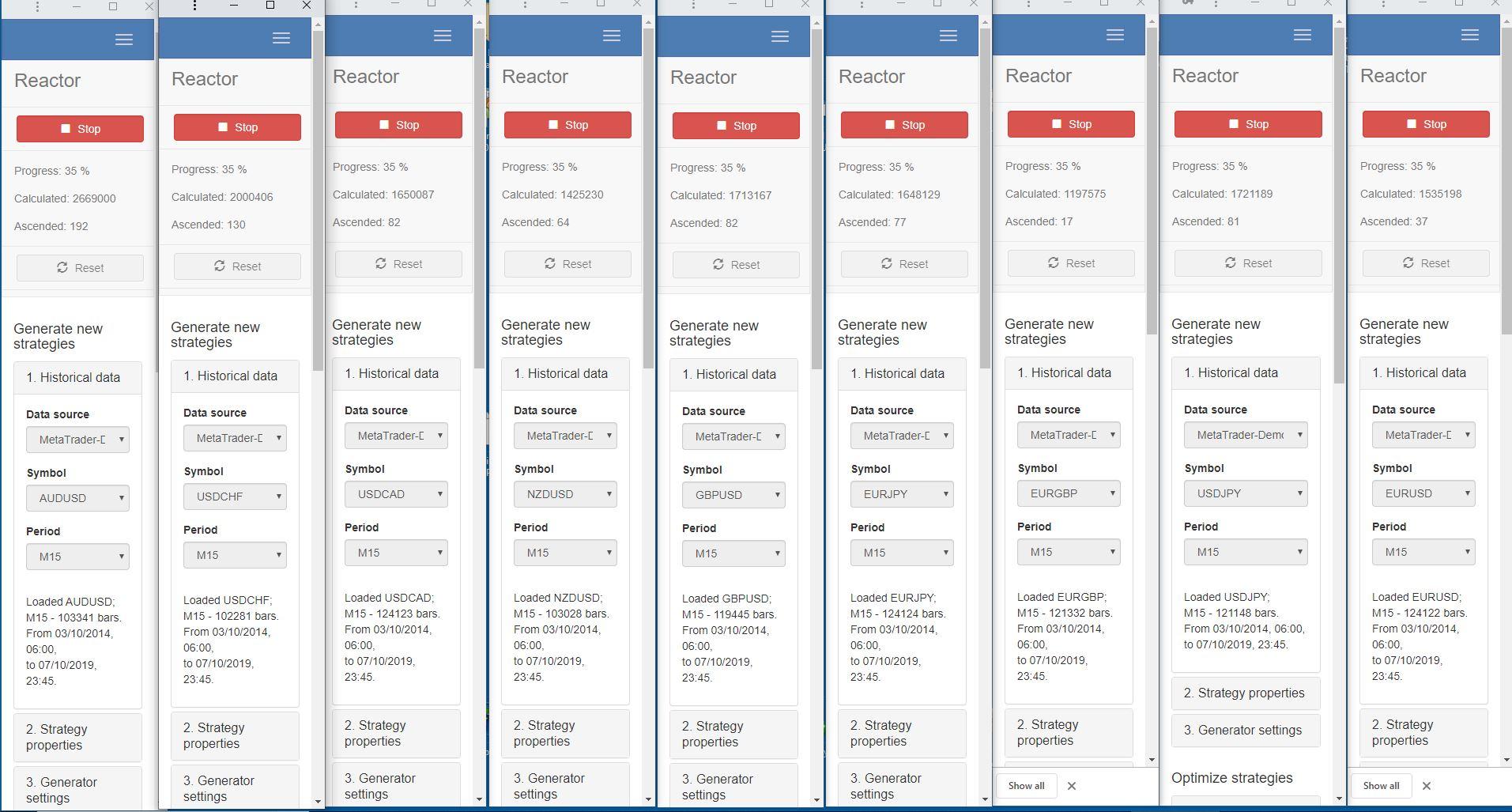

The reason why I asked this is because after generating strategies for 8 different currency pairs (with the same period of time, same number of bars, same timeframe, same parameters in the generator, same monte carlo, etc), 1 currency pair had 37 collected strategies while the rest was generating in between 10-20 strategies into the collection.

Additionally, I just want to mention that I ran EA Studio separately for the different currency pairs just to make sure the speed is not a factor that could have affected the number of generated strategies.

Cheers,

-

October 30, 2019 at 17:12 #25505champagnelennie44Participant

Good information and good advice.

Very useful.

-

October 30, 2019 at 22:20 #25519Petko AleksandrovKeymaster

Hello Jay-R,

You started a great topic here!

But it would be even more useful to the others and for you, if you share, for example, which currency pair exactly showed to you more strategies. This way the others will give it a try as well, and they will give you feedback.

That is my idea of the forum…a place where traders can share actual results from EAs, the generator, the reactor, and others to test it, feedback, test again…this way everyone will improve faster!!

Good job!

Kind regards,

Petko A -

October 31, 2019 at 5:45 #25541Jay-r YuzonParticipant

Hi Petko,

Yes, no problem. Here it is:

AUDUSD 37

EURGBP 15

EURJPY 18

EURUSD 21

GBPUSD 21

NZDUSD 22

USDCAD 15

USDCHF 9

USDJPY 13* I did not include EURCHF since the number of bars available to test were insufficient.

Historical data:

Source of data: Metatrader-Demo

Timeframe: M15

Testing periiod: More or less ending date is at 10/25/19

Bars: 100,000

Strategy Properties:

Lots: 0.01

SL: Always use. Fixed or Trailing. Range: 10-100

TP: Always use. Range: 10-100

Generator settings:

Working minutes: 500

Search best: Net Profit

OOS: 20%

Acceptance Criteria:

Complete Backtest

Min. Backtest Quality: 98

Min. Count of trades: 300

R-squared: 70

Profit factor: 1.2

In-Sample

Profit factor: 1.1

Out-of-sample

Profit factor 1.1

Monte Carlo:

Count of tests: 20

Validated tests: 80%

Monte Carlo tests:

BOTH tests under Strategy VariationI hope that helps.

Cheers,

-

October 31, 2019 at 8:13 #25551richardParticipant

Yes I get a lot of variation aswell. There is always variation in the “calculated” count as well. With some pairs getting twice as many as others…..

-

October 31, 2019 at 9:01 #25552Petko AleksandrovKeymaster

Hello guys,

I think that is quite normal to see different number of strategies because these are different markets.

Jay – R, on your Historical data:

Historical data:

Source of data: Metatrader-Demo

Timeframe: M15

Testing period: More or less ending date is at 10/25/19

Bars: 100,000You can increase the 100k bars:

Go to Data – Data Horizon – Maximum data bars.

You can increase the number from there. I normally keep it at 200k.

And with this data, you will get about 125k for M15. So you are just missing those 25k now.

Kind regards,

-

October 31, 2019 at 9:03 #25553Petko AleksandrovKeymaster

Hello Richart,

Do you run all of those Reactors on one and the same computer? Doesn’t your speed go down?

I normally keep it on 3-4 on one machine to keep up the good speed of the generator.

-

October 31, 2019 at 12:25 #25574richardParticipant

I’m running it on a pretty powerful PC. It had been running for 2 days to get those numbers. But yes it is probably too many to run. I’m just experimenting at the moment to see what the limits are…..

I’ll put that on the list of things to go over when we catch up tomorrow…..Cheers…..

-

-

October 31, 2019 at 11:08 #25568Jay-r YuzonParticipant

Thanks for pointing that out Petko. The number of bars for the M5 timeframe was actually hindering me from generating strategies for that

timeframe. Now that I actually have 200,000 bars, I’ll try it out.Yes, I was not surprised by the fact that other assets have different number of strategies generated into the collection given that the market is dynamic. Just curious though on what your take is on the quantity of the generated strategies in relation to its profitability. After generating strategies using the softwares for a good period of time, what does your experience have to say? Did you happen to observe any correlation between the quantity relative to the profitability?

Cheers,

-

November 1, 2019 at 10:05 #25685Petko AleksandrovKeymaster

Hello Jay-R,

I understand your point of view.

However, I do not think there is really a correlation in there. Even you notice some, it might be just a chance…

The question is that you would want to trade different assets for better risk-diversification. So even you get many strategies for AUDUSD and less for EURGBP, you would still want to trade the EURGBP. It is a different market, it will bring you extra pips.

Kind regards,

-

November 1, 2019 at 10:10 #25686Petko AleksandrovKeymaster

Hello Richard,

It is great to experiment. To have an idea if it goes slower, what you can do is to count the strategies.

For example, run those 9 reactors for 60 min, and see how many calculated strategies you have. After that run just the 3 of them for 60 min and see how many strategies you have.

Kind regards,

-

November 1, 2019 at 12:55 #25703Jay-r YuzonParticipant

Thanks Petko. It’s nice to have someone who has the experience to have his thoughts on this matter.

Yes, I’m definitely for risk-diversification as well.

Now that you’ve mentioned it, what are your thoughts if I’ll pair, say, AUDUSD and EURJPY? The reason why I’m asking especially with regards to these currency pairs is that although they are balanced—1USD, 1EUR, 1AUD, and 1JPY—AUDUSD has AUD (a risk currency), while EURJPY has JPY (a safe haven currency).

For my manual trading, I usually just trade either of the two in the event that there is a risk-on, risk-off mood in the market. As an algo trader who trades fully automated, would you proceed in trading these currency pair combinations simultaneously?

Kind regards,

-

November 2, 2019 at 19:42 #25840Petko AleksandrovKeymaster

Hello Jay-R,

it is really hard to give a precise answer to this question. I get your logic, but just try to ignore your experience (even it helps) in manual trading.

With the algorithmic trading, and especially with the strategies we use, you will notice that the market is different trough the eyes of EAs.

Yeah, I would trade those simultaneously. I do not see a reason why not to trade them with EAs…

Kind regards,

-

November 4, 2019 at 10:07 #25943Jay-r YuzonParticipant

I’ll keep in mind what you said Petko.

Thanks for all your help.

Sincerely,

-

November 6, 2019 at 9:01 #26155Petko AleksandrovKeymaster

No worries, Jay-R, just ask anything you feel uncertain about or curious.

I am happy when people ask questions :)

Cheers,

-

-

AuthorPosts

- You must be logged in to reply to this topic.