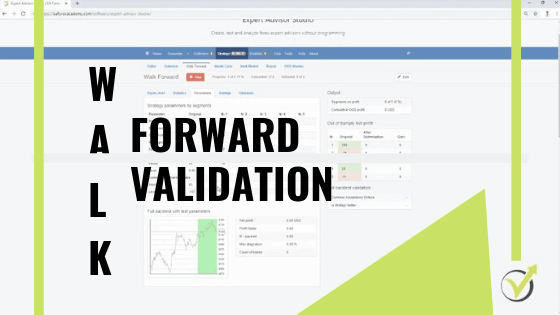

Walk Forward validation is a great robustness tool.

Hello dear traders, this is Petko Aleksandrov and I have decided to make an update because there was an update in the Walk Forward validation that is included in the Reactor in EA Studio.

And I wanted to make it clear how the Walk Forward validation work because many of the users and the traders of the Expert Advisor Studio and my students asked me to do such a video.

Now, if you actually go to Expert Advisor Studio, probably you have noticed that there are already the free videos that I have promised for some time. They are on the right side just below the login box.

So everybody who tests the software has the chance now to get these free videos.

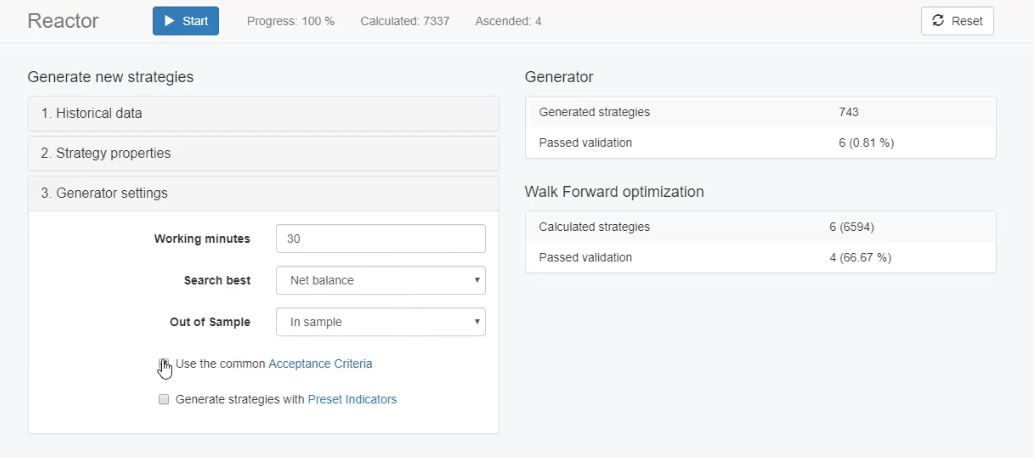

And this way it will be easier for one to start using the software faster. Now, if you go to the Reactor you will see that it is a generator plus robustness tools.

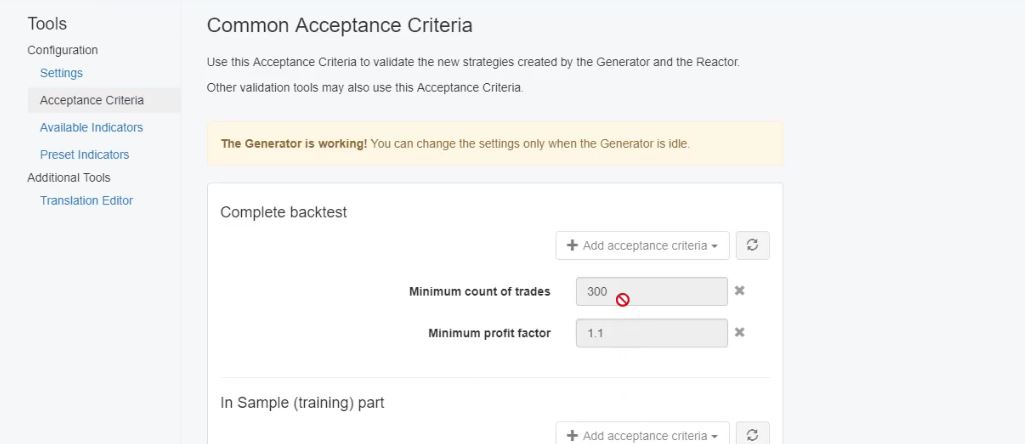

Acceptance criteria for the generator.

We can check the box if we want to use acceptance criteria:

With the Generator we can set acceptance criteria such as Profit Factor, Min Count of Trades, etc.

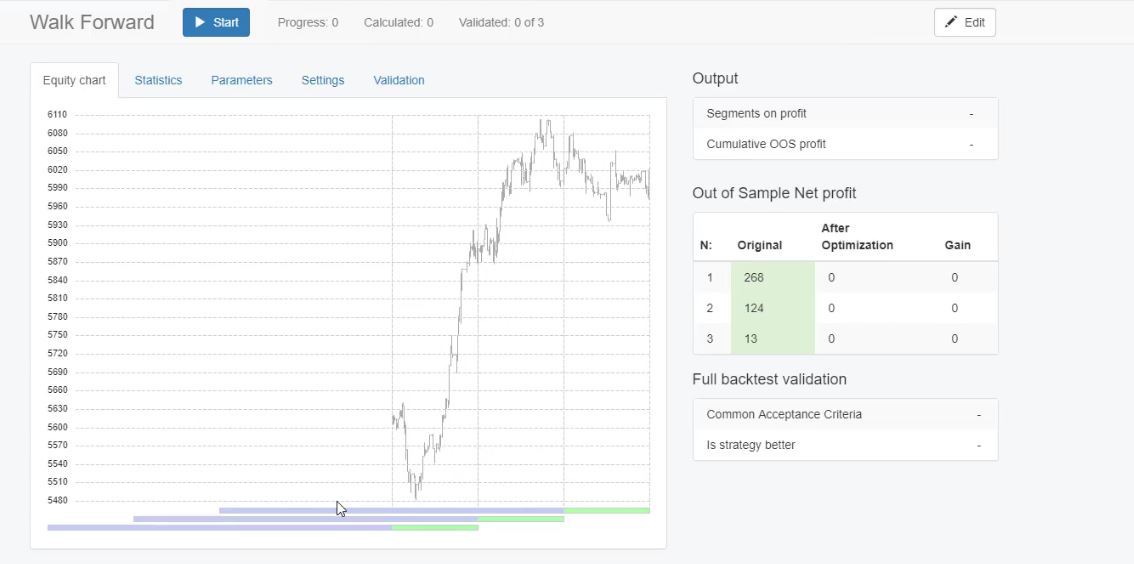

If the Generator is working on the complete historical data we have the chance to test the strategies with the Walk Forward validation:

This is the Out of Sample test. The difference now is that when the strategies are being generated with In Sample. In other words, we use the complete Historical data of bars.

When Out of Sample in the Walk Forward Validations isn’t placed.

So when the strategies are being generated, we can select them to go through the Walk Forward validation.

And the final backtest that we have with the Walk Forward validation, it does not use Out of Sample if Out of Sample is not placed in the Generator.

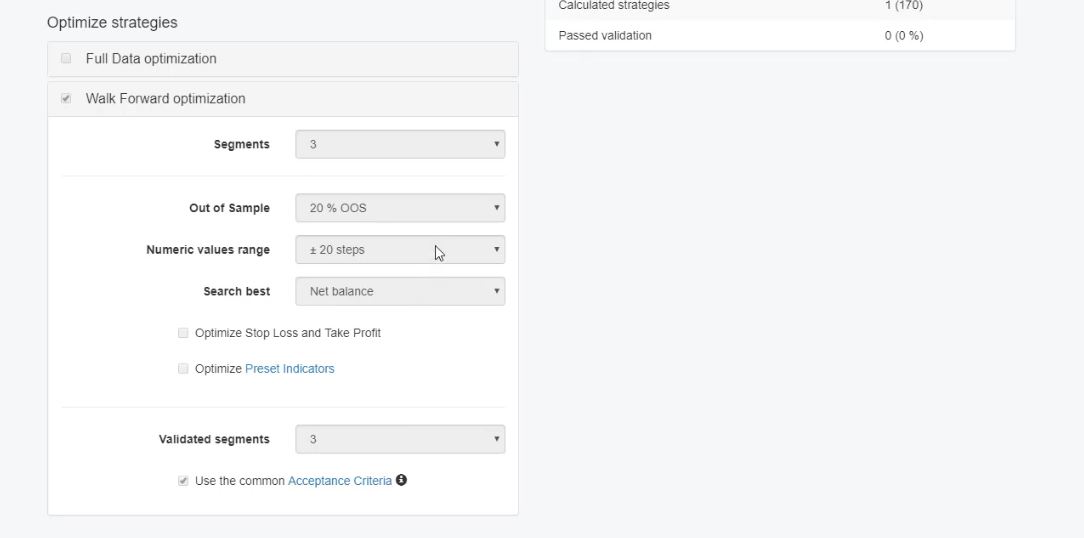

If in the Generator we don’t place Out of Sample, we stick with In Sample, the Walk Forward will do optimization with Out of Sample of 20%, for example, or any other percentage that you chose. But this will be for the different segments.

It will not be for the complete backtest at the end of the final backtest. The final backtest will use the Acceptance criteria which we selected. The settings are very similar. Actually they are the same as with full data optimization.

Performance of the final test according to how the strategy comes into the Walk Forward validation.

So this makes it just easier for the users. And as well, in the Walk Forward validation, we have the segments and then we have how many validated segments we want to have out of the total number.

And if we have in the In Sample, let’s say we select Out of Sample 20%, then the final backtest in the Walk Forward optimization will perform a backtest with Out of Sample. Or simply said, the way the strategy comes into the Walk Forward optimization, this is how the final test will be performed.

It doesn’t matter if it’s coming from the Generator, if it’s coming from the full data optimization where we have Out of Sample. And if we stick with In Sample in both the Generator settings and if we use full data optimization and in both places, you have In Sample.

As well the final test on the Walk Forward optimization will be without a green zone or simply said without Out of Sample.

And the Out of Sample that is in the Walk Forward optimization, this is for the segments. Let me go to the Editor and Walk Forward. It is for this thing over here, for this Out of Sample.

Feel free to ask questions about the Walk Forward Validation.

I know that the Walk Forward Validation is hard thing in algorithmic trading. But it is important and very useful to be used. Many traders use EA Studio without using the Walk Forward. Which is a pitty.

But if you use in the Generator In Sample, or if you decide to use the full data optimization and you choose In Sample, the Walk Forward validation will not do Out of Sample with the final backtest for the last parameters.

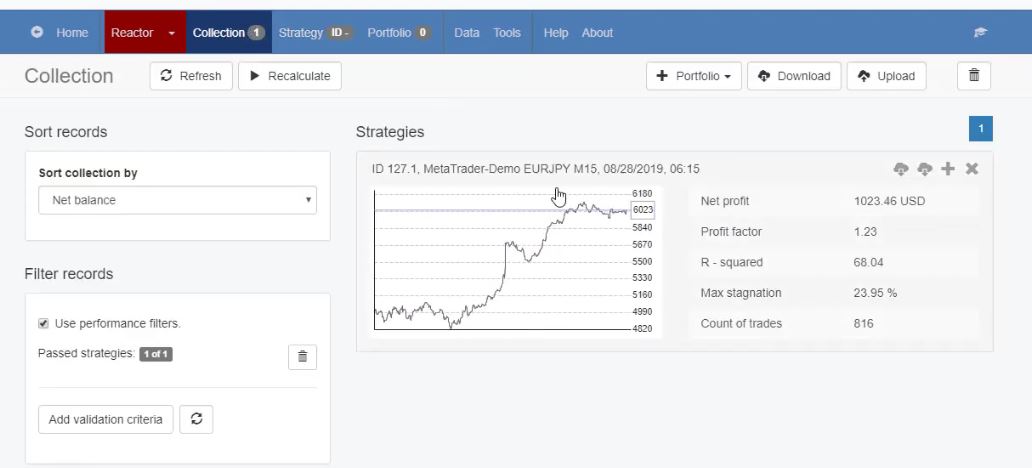

We have 1 strategy and there is no green zone anymore.

Basically, it is the very same thing as it was before. The difference is that the final backtest with the Walk Forward optimization is not done with Out of Sample anymore.

And it’s just the same thing. All we want to know is how the strategy performed with the last parameters from the last segment. So the Walk Forward does a backtest for the complete period.

If the strategy is better, if we have the common Acceptance criteria and if the segments are validated, we will see this strategy into the collection. So this is the difference. And this is the new thing here.

Feel free to ask me any questions if you have about the Walk Forward validation in the Forum.

Thank you for reading.

Cheers.